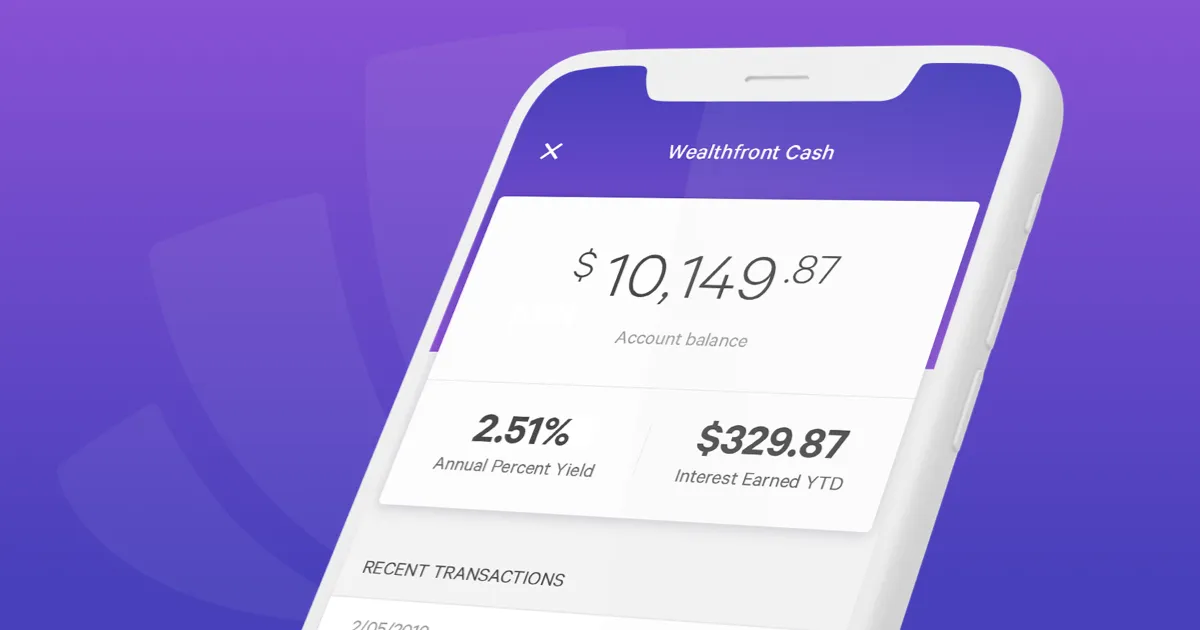

Why Wealthfront's Cash Account Is Not Safe

July 25th, 2019 · 8 min read

Have other articles like this sent directly to your inbox 📥

Sign up for my newsletter

Receive quality content on diverse topics. The premium edition, for free. 👊🏽

More articles from Nucks

What I Wish I Knew 5 Years Ago About Startups

Unbird began the Techstars Boulder 2019 startup accelerator program this week. I arrived with some skepticism and had questions about the value that would be generated from the program.

February 3rd, 2019 · 7 min read

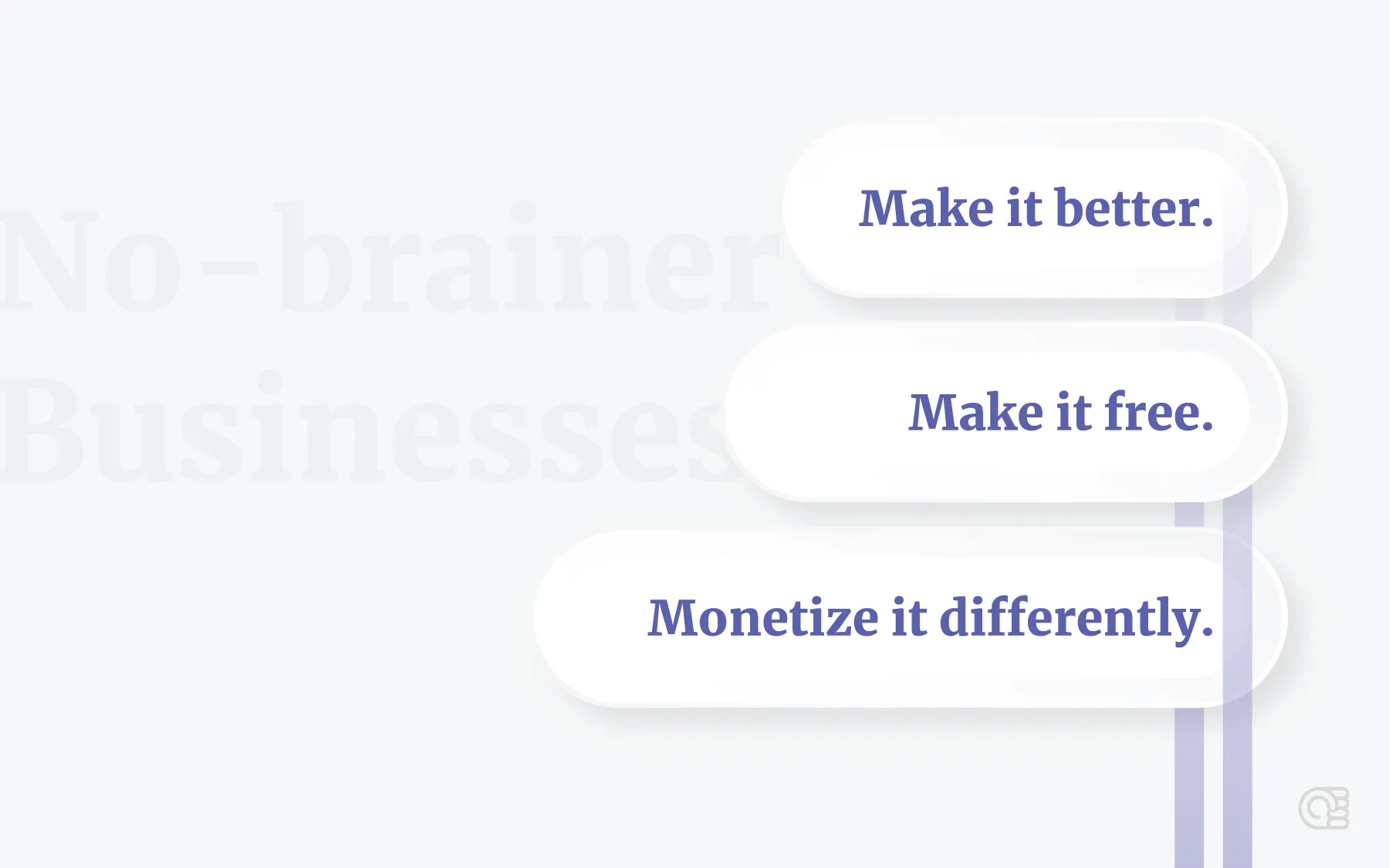

No-Brainer Businesses

October 20th, 2023 · 2 min read