Oct. 19, 2023: Since publishing this article in 2019, the company clarified its policies, and I am now comfortable keeping money with them.

In fact, I do. I highly recommend signing up for Wealthfront’s high-yield savings account, as it is one of the best options on the market.

If you want to explore why they were not safe at one point, feel free to read through this article.

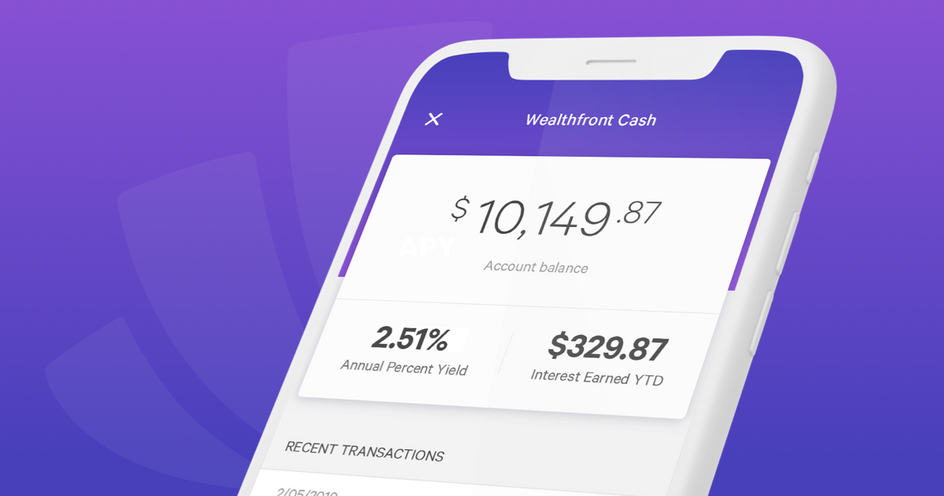

If you’re like me, you were excited to see an email in your inbox announcing that Wealthfront was increasing their interest rates again—from 2.50% APY to 2.57% APY. The gain was enough to rank Wealthfront #1 for the highest interest rate available for a savings account.

The increase wasn’t the largest jump but was enough to grab my attention, especially when I received an email the same week from Marcus telling me that they were about to lower their Savings Account rate from 2.25% APY rate to 2.15% APY.

Time to switch! Or so I thought.

![]()

What is Wealthfront?

Wealthfront is one of the largest robo-advisors on the market. They manage $15 billion in client investment assets and specialize in automating investment portfolios.

Due to their online business model, they can offer premium services with substantially lower costs than traditional financial advisors. According to company research, Wealthfront provides services to each client that would take roughly 105 hours for an investment manager to replicate. That’s a lot of hours!

Wealthfront’s offerings stand out to individuals who don’t want to bother with financial planning, forecasting or investing. If you would like to push a button and watch the money roll in, their accounts were designed for you.

One of their newest services is a high-yield cash account. Let me explain what that is before we dive into the dirty details of why you might not want to put your hard-earned cash into one of these accounts.

What a high-yield cash account can do for you

As the name suggests, high-interest or high-yield savings accounts are accounts that offer higher returns than standard savings accounts. They are generally safe vehicles to park your money and earn enough interest to keep up with inflation, if not beat it (which their rate does right now).

High-yield savings accounts are protected by the government (FDIC-insured) and generally offer $250k of protection should a bank fail. In other words, they are a great place to hold assets for short-term goals or emergencies.

Because Wealthfront is a brokerage and not a bank, their high-yield cash account is different from other high-yield savings accounts. Let’s begin with their interest rates.

How Wealthfront has higher rates than its competitors

At 2.32% annual percentage yield (APY), their cash account is nothing to gawk at.

They can offer such a competitive interest rate because they maintain zero physical locations which lower costs for the company. Steady income from other investment and advisory products they offer gives them additional leverage when setting their rates.

All banks set rates in accordance with the Federal Funds Rate, but as Wealthfront commonly publicizes, they try to go above and beyond to pass those savings on to their customers.

It’s hard not to believe those claims when Wealthfront increased their interest rate near the end of June while competitors lowered their rates that same week (and by the way, the Federal Funds rate didn’t change at all).

Wealthfront has out-priced other banks but hasn’t eliminated risks that other banks have eliminated. First, let me explain how they protect the money that you put into their savings accounts.

How Wealthfront is FDIC-insured without being a bank

One of the greatest protections provided by banks that offer savings accounts is FDIC insurance. Because Wealthfront is not a bank, they can only creatively extend this insurance—they split up your assets and deposit them for you into four separate banks. Wealthfront calls this their “Cash Sweep Program.”

By moving your assets into four financial institutions, Wealthfront can provide you with $1 million of FDIC insurance, far more than the average bank. In fact, no other bank gives this type of security. But with extra security comes added risks.

Why Wealthfront is riskier than other banks

1. Insecure funds

One downside to storing your money with Wealthfront is that they have to transfer your money to four banks to provide you with FDIC insurance. During the transfer your money is not FDIC-insured, meaning that if anything happened to it—if it were lost, misplaced, or stolen—the company would not be held liable.

Most individuals use savings accounts for money that they don’t want to risk losing, yet when opening an account with Wealthfront they are inherently agreeing to an opportunity to do so.

2. Lose control of your money

Before depositing money into Wealthfront’s high-yield cash account, you are required to sign an agreement called the Cash Sweep Program Disclosure Statement. This document is similar to a Terms & Conditions document, but it outlines practices by Wealthfront that you should be aware of regarding the movement of your money.

In the document, several circumstances are outlined that give Wealthfront the authority and permission to transfer your money into non-insured accounts without written approval. The circumstances described are as follows:

- If Wealthfront determines they need to protect your funds

- If partnering banks will not accept additional deposits

- If Wealthfront brokerage is unable to transfer your funds to a participating bank

- If a participating bank’s participation in the cash sweep program is terminated

- If a participating bank’s viability is in question

Given any of the above events, the agreement then says:

Under such circumstances and without prior notice to you, any or all of the Cash Balance in your Cash Account may be placed into a non-FDIC-insured bank, such as a money market mutual fund, a free credit balance position, or other available cash investment vehicle. These alternative cash sweep options would not be eligible for FDIC insurance but may be eligible for SIPC protection. Your continued use of your Cash Account following such change to your cash sweep option shall constitute your consent to any such change.

In other words, Wealthfront can legally move your money into non-insured banks without talking to you about it. That may be a risk that some are unwilling to make.

The pros and cons of using Wealthfront might also be useful when considering whether or not the risks are worth taking.

The pros of using Wealthfront

- They have the highest interest rate available for a savings account (now 2.32%).

- Their app is modern & makes it so you can easily access your account information on the go.

- They offer a ”Plan” feature for free which helps you document money goals and track their progress.

- The website has one of the most simple and clean user interfaces I’ve seen with great design.

- You can keep all of your money under the management of one company if you use them for planning, saving, and investing.

- A support team is available to contact online.

- Your first $5,000 of investments managed for free with a referral.

The cons of using Wealthfront

- Money transferred into a savings account cannot be directly moved into a Wealthfront investment account.

- No automated transfers. You cannot deposit money directly from other accounts into Wealthfront on specific schedules.

- Funds are not always secure.

- You lose control of your money.

- No physical locations or branches are available.

Conclusion

Although Wealthfront has the highest interest rates on the market, their high-yield cash accounts are not for every saver. If you are still interested in earning more after acknowledging the risks, you can open a Wealthfront high-yield cash account here.

Or, if you’d rather investigate your options further, I put together a comprehensive list of high-yield savings accounts along with their interest rates and information about each bank for you to reference.

May 23, 2020: Because of the volatility of interest rates, this article may not reflect the actual APY offered by Wealthfront. Know that the rest of the article contains pertinent information and is not outdated, even though the rates may be.

Feb. 10, 2023: Wealthfront clarified in Nov. 2022 that your deposited money is insured by SIPC during transit. In other words, funds are fully protected up to the limits that Wealthfront specifies on its website.